Blog

Samuel Leeds Buys Shares In Property Tribes; Says He Wants To Make It Better

People in UK property circles may be familiar with the very public dispute between former MTV presenter, property investor, and community manager of the company Property Tribes, Vanessa Warwick, & property investment trainer and owner of the company ‘Property Investors’, Samuel Leeds; as Leeds has accused Warwick of assisting with racism and discrimination against ethnic minority tenants. In recent news, Samuel Leeds was reported to have bought a 35% share of the company Property Tribes, making him officially now a person of significant control at Property Tribes.

Warwick established Property Tribes to accumulate wisdom from various property owners and landlords to create a place of guidance for people in the industry to do business better. According to the company,

“We wanted to create a free use, safe, and agenda-free place for landlords to get information from a “hive mind”, not a singularity, so that they could learn and grow their property business.”

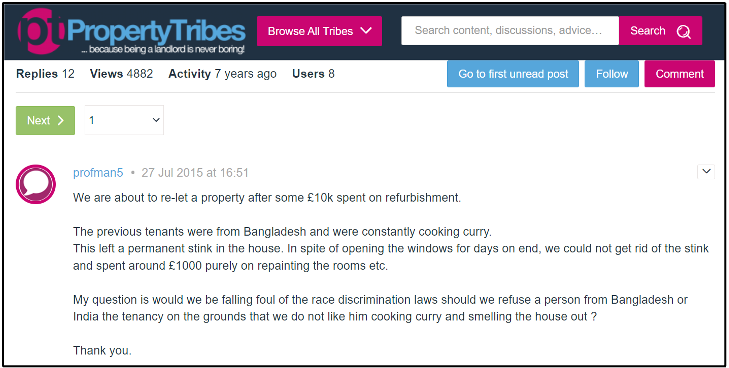

However, in one of his recent videos, Samuel Leeds pointed out blatant support of racism in some of the advice coming from Warwick herself. As one of the landlords asks on the forum – if they would be implicated by the race discrimination laws in the UK for refusing tenancy to Bangladeshi families as the landlord is not fond of the smell of their staple food, curry; Vanessa Warwick herself is seen advising against mentioning the reason for said refusal, thus averting the legal repercussions altogether.

In the video, Leeds points out several more situations where Warwick has behaved in a racist manner. In fact, she has become a new advisor on the panel of the UK’s Property Redress Scheme and has been under criticism in their forum as well for supporting discrimination against ethnic minorities.

Warwick also expressed strong disapproval of Leeds as a property trainer citing the reason that his students came from the “vulnerable” demographic. Leeds called out the racist mindset in this reasoning, as in reality, his students predominantly come from ethnic minorities and don’t fall in the “vulnerable” category. He began drawing attention to the issue over his YouTube channel and his website, and ended up facing severe disparagement from Warwick and her followers. Leeds finally sued Warwick for defamation and she brought a counter lawsuit for six-figure damages.

In an attempt to put an end to the battle once and for all, Samuel Leeds reports to have bought a share, 35% to be exact, of the company, Property Tribes. Even though he is only a minority shareholder and will have limited control, Leeds believes he can make a difference in “cleaning up the company” and reduce racism in the forum.

He jokingly adds,

“Because they trolled me, I wanted to at least get paid… Like Michael Jackson did to Eminem.”

Leeds pledges that any money he makes off this transaction will be donated to charitable organisations that tackle racism and online bullying. In addition, Leeds will donate an extra £50,000 to organisations that fight hatred in the UK. With this move, he is determined to take a strong stand against all discriminations in the property sector or any other industry.

Une plateforme pensée pour les joueurs exigeants

Vive Mon Casino s’affirme en 2026 comme une plateforme de jeux en ligne fiable, adaptée aux besoins d’un large public francophone. L’expérience utilisateur et la gestion de l’argent y occupent une place centrale dans la stratégie du site. Parmi les critères essentiels pour tout joueur sérieux, la rapidité des retraits est souvent décisive pour juger de la qualité d’un casino en ligne. Dans cet article, nous analysons en détail le délai moyen de retrait chez Vive Mon Casino, en tenant compte des méthodes de paiement, des vérifications imposées et des pratiques du marché en 2026.

Pour consulter directement la plateforme, vous pouvez visiter moncasino et découvrir les options disponibles.

Quelle est la réalité du délai de retrait chez Vive Mon Casino ?

Le délai de traitement des retraits chez Vive Mon Casino est un facteur clé pour la satisfaction des joueurs. En 2026, la plateforme propose plusieurs méthodes de retrait, chacune avec ses particularités en termes de rapidité et de commodité.

Voici les détails pratiques des délais moyens observés :

| Méthode de retrait | Délai moyen de traitement | Particularités principales |

|---|---|---|

| Virements bancaires | 3 à 5 jours ouvrés | Sécurité accrue, délais variables selon banque |

| Portefeuilles électroniques (e-wallets) | 1 à 24 heures | Rapidité optimale, popularité croissante |

| Cartes bancaires | 2 à 4 jours ouvrés | Procédures bancaires standard |

| Cryptomonnaies | Quelques minutes à 2 heures | Frais faibles, anonymat, instantané dans la plupart des cas |

Le casino traite généralement les demandes de retrait sous 24 heures, mais le temps final dépend aussi des vérifications d’identité et du mode choisi. Vive Mon Casino mise sur la transparence, avec un suivi clair des demandes et une communication active sur l’avancement du traitement.

Pourquoi ces délais sont-ils compétitifs sur le marché ?

Comparé à d’autres casinos en ligne, Vive Mon Casino propose des délais de retrait qui se placent dans la moyenne haute, voire au-dessus, particulièrement pour les portefeuilles électroniques et les cryptomonnaies. Cela s’explique par :

- Une plateforme optimisée pour l’efficacité des transactions.

- Des procédures KYC (Know Your Customer) simplifiées sans compromettre la sécurité.

- Une large variété de moyens de paiement adaptés aux besoins du marché européen et francophone.

Sur le plan comparatif, la majorité des casinos exigent souvent de 2 à 5 jours ouvrables pour valider une demande, voire plus en cas de contrôle renforcé. Les portefeuilles électroniques restent la méthode la plus rapide, comme cela est également le cas chez Vive Mon Casino.

Focus sur les étapes qui influencent le délai de retrait

Le temps d’attente ne se limite pas au simple transfert d’argent. Plusieurs phases impactent les délais :

- Vérification du compte : obligatoire avant tout premier retrait, elle peut prendre de quelques heures à un jour.

- Validation de la demande : le support et le système automatisé analysent la demande en moins de 24 heures.

- Traitement bancaire ou transfert : selon la méthode, cette étape est la plus variable.

- Réception des fonds par le joueur : enfin, la durée dépend des intermédiaires financiers.

Pour un joueur régulier, ces étapes sont fluidifiées grâce à la fidélisation et la documentation déjà validée, ce qui accélère les retraits suivants.

À retenir : avantages et subtilités de Vive Mon Casino

- Délai moyen de traitement estimé entre quelques minutes (cryptomonnaies) et 5 jours (virement bancaire).

- Priorité donnée aux solutions rapides comme les portefeuilles électroniques.

- Système sécurisé intégrant des contrôles stricts, mais simplifiés pour éviter les longs blocages.

- Transparence et support disponible pour accompagner les demandes.

Tableau récapitulatif des délais moyens 2026

| Moyen de retrait | Rapidité moyenne | Note sur la rapidité* |

|---|---|---|

| Cryptomonnaies | 15 minutes à 2 heures | ★★★★★ (très rapide) |

| Portefeuilles électroniques | 1 à 24 heures | ★★★★☆ (rapide) |

| Cartes bancaires | 2 à 4 jours ouvrés | ★★★☆☆ (standard) |

| Virements bancaires | 3 à 5 jours ouvrés | ★★☆☆☆ (lent comparé aux autres) |

*Note basée sur la moyenne du marché iGaming européen en 2026

FAQ – Vos questions sur les délais de retrait chez Vive Mon Casino

Q1 : Vais-je toujours devoir attendre plusieurs jours pour retirer mes gains ?

Non, cela dépend du mode de retrait choisi. Les cryptomonnaies et e-wallets permettent souvent des retraits quasi immédiats.

Q2 : Le casino impose-t-il des limites de retrait qui ralentissent le processus ?

Vive Mon Casino applique des plafonds selon le statut du joueur, mais ceux-ci sont clairement annoncés et n’allongent pas les délais de traitement si les demandes sont conformes.

Q3 : Que faire si mon retrait prend plus de temps que prévu ?

Le support client est disponible 24/7. Vous pouvez le contacter via chat en direct ou email pour obtenir un suivi personnalisé.

Q4 : Le délai est-il le même pour un joueur nouveau et un joueur VIP ?

Les joueurs VIP bénéficient souvent d’un traitement prioritaire, ce qui peut réduire significativement les délais.

Q5 : Les documents fournis influencent-ils la rapidité du retrait ?

Oui, un dossier complet et conforme permet de gagner du temps sur la vérification KYC et accélère le processus global.

En conclusion, Vive Mon Casino s’impose en 2026 comme une plateforme qui combine sécurité et rapidité des transactions, avec un délai moyen de retrait très compétitif selon les standards du marché. Pour ceux qui privilégient la rapidité, les solutions électroniques et blockchain offrent des avantages considérables, tandis que les méthodes classiques restent fiables et transparentes. Ce positionnement fait de Vive Mon Casino un choix sûr pour jouer en toute sérénité tout en gardant un contrôle rapide sur ses gains.

-

Tech5 years ago

Tech5 years agoEffuel Reviews (2021) – Effuel ECO OBD2 Saves Fuel, and Reduce Gas Cost? Effuel Customer Reviews

-

Tech7 years ago

Tech7 years agoBosch Power Tools India Launches ‘Cordless Matlab Bosch’ Campaign to Demonstrate the Power of Cordless

-

Lifestyle7 years ago

Lifestyle7 years agoCatholic Cases App brings Church’s Moral Teachings to Androids and iPhones

-

Lifestyle5 years ago

Lifestyle5 years agoEast Side Hype x Billionaire Boys Club. Hottest New Streetwear Releases in Utah.

-

Tech7 years ago

Tech7 years agoCloud Buyers & Investors to Profit in the Future

-

Lifestyle6 years ago

Lifestyle6 years agoThe Midas of Cosmetic Dermatology: Dr. Simon Ourian

-

Health7 years ago

Health7 years agoCBDistillery Review: Is it a scam?

-

Entertainment7 years ago

Entertainment7 years agoAvengers Endgame now Available on 123Movies for Download & Streaming for Free